2016/03/09 - Walter's Blog: TIF Questions and Rasp Farm

Tax Increment Financing Questions

March 9, 2016

There has been an article and questions lately about the so-called Rasp Farm Tax Increment Financing (TIF) project. Everyone is entitled to their opinions and objections about this project and about TIF, but first and foremost I want to clarify that the City’s activities with the Rasp Farm TIF have been in accordance with the TIF Plan approved by the City Council and with state TIF law.

I also want to remind everyone that the City Council’s purpose for the Rasp Farm TIF was to alleviate the significant flooding problem in the Southview Gardens subdivision, particularly along Dartmouth and Laverna Evans Elementary School. By that standard, the project is a success. Here is a picture of what Dartmouth used to look like during heavy rains:

Since the Rasp Farm TIF project was approved and TIF funds were used to make drainage improvements, there have been no major flooding problems in Southview Gardens or around Laverna Evans School.

This project came together in 2010. Flooding had long been a problem in Southview Gardens and the source was water coming off of I-64 and through the Rasp Farm property along South Lincoln. At the time, the property was actually within the boundaries of the Village of Shiloh and proposed for apartment buildings. Southview Gardens residents did not want the apartments and the City of O’Fallon had neither the jurisdiction to stop the apartments nor the money to fix the flooding problems.

A developer was interested in building something else on the property, but the property needed to be annexed to O’Fallon and the flooding improvements needed were far beyond what our ordinances would require the developer to do. The City of O’Fallon could not afford to fix the flooding so we investigated creative solutions.

It turned out there was a TIF District nearby that had already completed all of its infrastructure improvements but still had eight years left of its 23-year life span. The City Council agreed that it would be a good use of TIF funds to expand the boundaries of the TIF District to include the Rasp Farm so that the flooding could be fixed without raising city-wide property taxes and without creating a new TIF District. This way, the Rasp Farm TIF would only be in effect for eight years rather than the 23 years possible in the state TIF law and the other taxing bodies (such as school districts) would receive the full effect of the property taxes sooner.

The TIF Funds have paid $2.6 million to the developer for the project so far. Around $1 million was spent (and reimbursed to the developer) for drainage improvements and infrastructure and the remainder was for property acquisition. Some people are critical about using TIF funds for land purchase, but it is allowed in the state TIF law and was approved by the City Council in the TIF Plan. After all, the entire 52 acres had to be purchased to make the required infrastructure improvements and build the detention pond.

The newspaper article correctly explains that the property has yet to develop, which is unfortunate. It is also accurate that the developer has not received any payments for the past two years: the TIF Plan requires the developer to demolish the strip center and build an intersection with turn lanes and traffic signals. The work has not been done, so the City is holding $743,482.65 in payments to the developer until this is accomplished.

The justification for the TIF was to relieve chronic flooding in the Southview Gardens neighborhood and Laverna Evans School, and that was accomplished. We expected the office park to develop sooner, but neither the City nor any developer can control the market.

The TIF Plan is on the City’s web site. You can view maps, Frequently Asked Questions, contact information, and extensive legal language that justifies the use of TIF for this project.

TIF FAQ

This may be more than anyone wants to know about TIF, but here is an attempt to answer some of the basic questions related to TIF and how it functions. There is a state statute that governs how TIF can be used and what qualifies for TIF funding.

The majority of my information comes from a report by the City of Chicago’s TIF Reform Panel that was published on August 21, 2011. (Here is the link to the full report: please note that the “Analysis of Illinois TIF Act” actually begins on Page 67. The first 66 pages are an analysis of TIF in the City of Chicago.)

What is TIF?

Tax Increment Financing is a local economic development tool created under state law to enable units of local government to encourage and facilitate public and private investment in the development or redevelopment of areas located within the municipality that meet certain conditions of blight, decay or underperformance. The TIF structure enables a municipality to stimulate new private investment in the development or redevelopment of an area. The investment is accomplished by providing financial support to redevelopment projects that address “blighted areas” or treat and improve “conservation areas” and “industrial park conservation areas.”

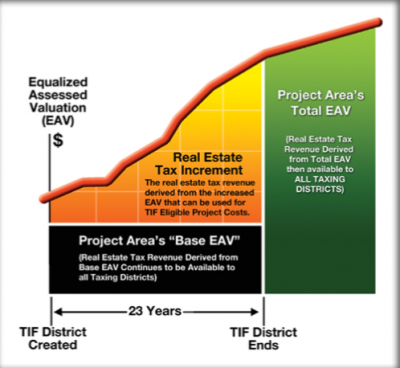

How does TIF work?

A tax increment is the difference between the amount of property tax revenue generated before TIF district designation (base) and the amount of property tax revenue generated after TIF designation (increase).

Source: www.tifillinois.com

Once a TIF District is established, the tax increment for that property is collected and placed in a TIF fund. TIF funds can be used to help pay for public improvement projects or other TIF eligible improvements on the property.

Property values are reevaluated every two years in connection with the property tax reassessment process. All of the overlapping taxing bodies continue to receive property tax revenue from the base amount of taxes, so there is no loss of revenue to those local taxing bodies.

The maximum life of a TIF District is 23 years. When the TIF ends, the total amount of tax revenues are again shared by all the taxing bodies. At the end of the TIF, the total amount should be larger than from before the TIF, due to the growth which would not have been possible without the utilization of Tax Increment Financing.

What does it do to property taxes?

For residents and property outside of the TIF area, there are no changes to their property taxes. Property owners within the TIF area will pay normal property taxes, but the increment will go back into the project instead of to the taxing bodies. The state TIF law specifies what TIF funds can be used for.

How is a property qualified for TIF?

Under the TIF Act, a "blighted area" can be any improved or vacant area within the boundaries of a redevelopment project area located within the territorial limits of the municipality where:

(1) If the area is improved, the improvements include industrial, commercial, and residential buildings or other improvements that are detrimental to the public safety, health, or welfare because of a combination of 5 or more factors, each of which must be (A) present, with that presence documented, to a meaningful extent so that a municipality may reasonably find that the factor is clearly present within the intent of the TIF Act and (B) reasonably distributed throughout the improved part of the redevelopment project area.

The possible factors include

- Dilapidation

- Inadequate utilities

- Obsolescence

- Excessive land coverage and overcrowding of structures and community facilities

- Deterioration

- Deleterious land use or layout

- Presence of structures below minimum code standards

- Environmental clean‐up

- Illegal use of individual structures

- Lack of community planning

- Excessive vacancies

- Declining or relatively inadequate total equalized assessed value in 3 of the last 5 calendar years

- Lack of ventilation, light, or sanitary facilities

(2) If the area is vacant, the sound growth of the redevelopment project area is impaired by a combination of 2 or more factors from Group A below or one factor from Group B below, each of which (in either case) is (A) present, with that presence documented, to a meaningful extent so that a municipality may reasonably find that the factor is clearly present within the intent of the Act and (B) reasonably distributed throughout the vacant part of the redevelopment project area. The TIF Act expressly provides that in defining a blighted area, the term "vacant land" means any parcel or combination of parcels of real property without industrial, commercial, and residential buildings that has not been used for commercial agricultural purposes within five years before the designation of a redevelopment project area unless the parcel is included in an industrial park conservation area or has been subdivided.

Group A

- Obsolete platting of vacant land

- Deterioration of structures or site improvements in neighboring areas adjacent to the vacant land

- Diversity of ownership of parcels of vacant land

- A need for environmental remediation, provided the remediation costs constitute a material impediment to the development or redevelopment of the redevelopment project area

- Tax and special assessment delinquencies or tax sales

- Declining or relatively inadequate total equalized assessed value in3 of the last 5 calendar years

Group B

- Area consists of one or more unused quarries, mines, or strip mine ponds

- Area consists of an unused or illegal disposal site containing earth, stone, building debris, or similar materials that were removed from construction, demolition, excavation, or dredge sites

- Area consists of unused railyards, rail tracks, or railroad rights‐of-way

- Area qualified as a blighted improved area immediately prior to becoming vacant, unless there has been substantial private investment in the immediately surrounding area

- Area is subject to chronic flooding that adversely impacts on real property in the area

What can TIF funds be used for?

The TIF Act provides that the revenue generated in a TIF District can be used to pay or reimburse redevelopment project costs – costs that are reasonable or necessary costs incurred or estimated to be incurred or that are incidental to a redevelopment plan and a redevelopment project. The TIF Act specifies several eligible uses, but also provides that the list is not inclusive of all eligible costs. Generally (with some restrictions), the revenue may be used for costs relating to the administration of the TIF redevelopment project, studies, surveys and plans, property acquisition, demolition and site preparation, the rehabilitation or renovation of existing public or private buildings, the construction of public works or improvements, job training, relocation expenses, financing costs (including interest write-down), the marketing of sites within the TIF District and professional services, such as architectural, engineering, legal, and financial planning. Specifically excluded are costs of construction of new private buildings and municipal buildings providing certain services unrelated to the TIF District. Again, the threshold requirement is that the costs qualify as a redevelopment project cost under the TIF Act.

Typical projects include:

- The redevelopment of substandard, obsolete, or vacant buildings

- Financing general public infrastructure improvements, including streets, sewer, water, and the like, in declining areas

- The development of residential housing in areas of need

- Cleaning up polluted areas

- Improving the viability of downtown business districts

- Providing infrastructure needed to develop a site for new industrial or commercial use

- Rehabilitating historic properties.