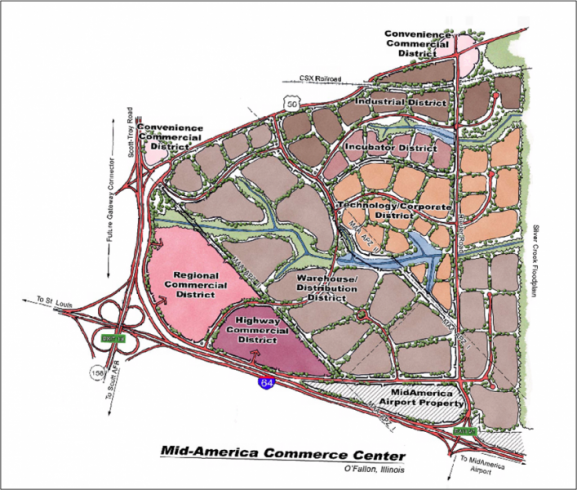

MidAmerica Enterprise Zone

Ord #3838- 2014 Expansion

Ord #3801 - 2013 Expansion

Enterprise Zones are among Illinois' most important tools to stimulate economic growth and neighborhood revitalization. The Enterprise Zone program depends upon a creative partnership between state and local government, businesses, labor and community groups to encouage economic growth in the areas desgnated as Enterprise Zones. Although the program is administered at the state level by the Department of Commerce and Community Affairs (DCCA), its ultimate success depends on the level of local commitment.

There are currently 93 Enterprise Zones in Illinois, the maximum number that may be designated according to Illinois law. All offer the same mix of state incentives designed to encourage companies to locate or expand within a zone. In addition, each zone offers distinctive local incentives to enhance business or neighborhood development efforts. Such local incentives include abatement of property taxes on new improvements, homesteading and shopsteading programs, waiver of business licensing and permit fees, streamlined building code and zoning requirements, and special local financing programs and resources.

For more information on available properties, click here.

Please view our interactive GIS map to determine if your property is within one of our TIF districts or Enterprise Zone.

State Incentives

Sales Tax Exemption - A 6.25 percent state sales tax exemption is permitted on building materials to be used in an Enterprise Zone. Materials must be permanently affixed to the property and must be purchased from a retailer located within the boundaries of the unit fo government sponsoring the enterprise zone.

Enterprise Zone Machinery and Equipment Consumables/ Pollution Control Facilities Sales Tax Exemption - A 6.25 percent state sales tax exemption on purchases of tangible personal property to be used in the manufacturing or assembly process or in the operation of a pollution control facility within an Enterprise Zone is available. Eligibility is based on a business making an investment in an Enterprise Zone of at least $5 million in qualified property that creates a minimum of 200 full-time-equivalent jobs, a business investing at least $40 million in a zone and retaining at least 2,000 jobs, or a business investing at least $40 million in a zone which causes the retention of at least 90 percent of the jobs existing on the date it is certified to receive the exemption.

Enterprise Zone Utility Tax Exemption - A state utility tax exemption on gas, electricity, and the Illinois Commerce Commission's administrative charge and telecommunication excise tax is available to businesses located in Enterprise Zones. Eligible businesses must make an investment of at least $5 million in qualified property that creates a minimum of 200 full-time- equivalent jobs, or an investment of $175 million that creates 150 full -time-equivalent jobs in Illinois. The majority of the jobs created must be located in the Enterprise Zone where the investment occurs.

Enterprise Zone Investment Tax Credit - A state investment tax credit of 0.5 percent is allowed a taxpayer who invests in qualified property in a Zone. Qualified property includes machinery, equipment and buildings. The credit may be carried forward for up to five years. This credit is in addition to the regular 0.5 percent investment tax credit, which is available throughout the state, and up to 0.5 percent credit for increased employment over the previous year.

Dividend Income Deduction - Individuals, corporations, trusts, and estates are not taxed on dividend income from corporations doing substantially all their business in an Enterprise Zone.

Jobs Tax Credit - The Enterprise Zone Jobs Tax Credit allows a business a $500 credit on Illinois income taxes for each job created in the Zone for which a certified eligible worker is hired. The credit may be carried forward for up to five years. A minimum of five workers must be hired to qualify for the credit. The credit is effective for people hired on or after January 1, 1986.

Interest Deduction - Financial institutions are not taxed on the interest received on loans for development within an Enterprise Zone.

Contribution Deduction - Business may deduct double the value of a cash or in-kind contribution an approved project of a designated Zone organization from taxable income.