2023/03/29 - Walter's Blog: Budget Part 2-Revenue

I previously wrote about how our annual budget is structured. This time I will discuss our revenue situation. As we continue to recover from the COVID-19 pandemic, most of our local revenue sources are improving. 95% of residents said that O’Fallon is a great place to live in our recent Citizen Survey, and this budget will continue to provide high quality services to the community.

The budget reflects expenditures in all funds of $103,546,657, which are equally balanced by revenues. Where possible, we have included the City Council’s priorities from the 2040 Master Plan to guide our budget decisions. The Master Plan is culmination of 18 months of input from residents, City Council, and staff to direct the City of O’Fallon’s activities over the next 20 years. A component of the Master Plan is a Strategic Plan that identifies action steps over the next 3-5 years. The Capital Improvement Plan (CIP) incorporates Strategic Plan projects and other equipment and construction projects into the next five years.

The Strategic Plan and CIP served as the planning documents for this proposed budget. This budget was programmed around these goals and through direct input from the Mayor and Council, Staff, and refinement through City Council committee review.

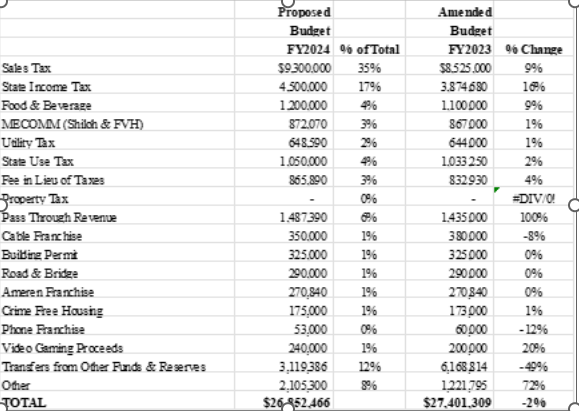

The General Fund is the main fund for the City, and it provides the budgets for Administration, Police, Community Development, Streets, Facilities, Finance, Police and Fire Commission, Cemetery, Information Technology, and 911 Dispatch (MECOMM) departments. General Fund revenue is estimated to decrease approximately 2%, mainly because there are no ARPA Funds (American Rescue Plan Act) in this budget. The revenue for the General Fund is proposed to be derived as follows:

Sales tax comprises the largest part of the General Fund (35%). Sales tax revenues for FY2024 are estimated to be slightly higher than the FY2023 budget. A strong economy and new businesses have helped offset the loss of revenue due to the relocation of the Auffenberg Auto Mall.

The State Income Tax is the City’s second largest revenue source and is expected to increase. The tax is funded on a per capita basis, so our allocation from the Sales Tax has increased due to O’Fallon’s population increase from the 2020 Census. The State Income Tax is subject to the state government’s annual budget and is subject to fluctuate depending on the state’s budget situation. The state government reduced the State Income Tax distribution to local government by 10% in 2018 and was never restored. As of the approval of this budget, the state’s budget has not been approved and there is no assurance that the State Income Tax level will be restored.

Property taxes are levied for the Library, Emergency Medical Services, Fire Department, and employee pension funds. Property tax levies were eliminated last year from the budget for the General Fund and Park Fund as part of a Property Tax Relief Program and the creation of the Build O’Fallon Trust Fund. The Property Tax Relief Program eliminated the property tax levies for the General Fund and Park Fund and increased the Sales Tax by ½%.

Half of the Sales Tax increase is allocated to the Park Fund to replace the property tax levy. The other half of the Sales Tax increase is allocated to the Build O’Fallon Trust Fund, which is a special account for the City Council to implement the Master Plan.

The Food & Beverage Tax declined significantly during the pandemic but has rebounded since the reopening eating establishments and new restaurants.

The “Fee in Lieu of Taxes” represents the portion of administrative salaries and benefits that were originally reflected in the Enterprise Funds (Water and Sewer). State law requires that municipal utilities charge an administrative fee, so they are similar to private sector utilities that must pay property taxes and utility taxes.

The Utility Tax is a tariff that is based on consumption and not the actual rate. Warm winters and cool summers can significantly affect Utility Tax. A large portion of the Utility Tax is committed to paying off the $7 million Public Safety Facility that was completed in 2004. The remainder is used to fund the Parks and Recreation Department.

The Hotel/Motel Tax suffered the most during the pandemic but has since recovered. Hotels had a great year last year, and we expect another strong year for the Hotel/Motel Tax.

In summary, the City’s revenue situation is stable and growing, although we are concerned about possible economic changes due to inflation, bank instability, or international conflicts. In my next blog, I will address our expenses in the annual budget and how it reflects the priorities identified by the City Council.